Structured

Settlement Companies

Sell your settlement and get $500

within 24 hours.*

What is a Structured Settlement Company?

A structured settlement company is either a broker that helps set up payment streams to meet legal requirements or a buyer that purchases structured settlements.

What is a Structured Settlement Buyer?

A structured settlement buyer is a company that provides cash up front to people with structured settlements in exchange for rights to future payments. These factoring companies normally buy future payments rights from structured settlements and annuity holders.

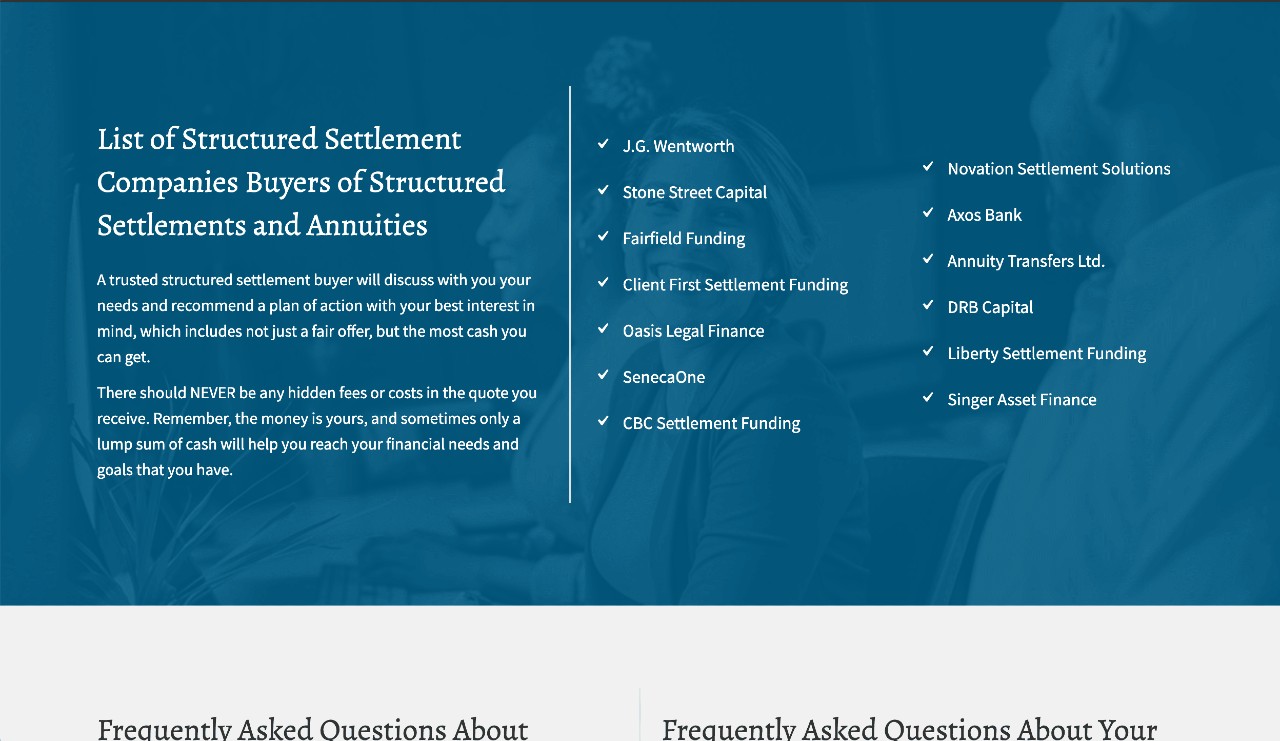

Who Buys Structured Settlements?

Many companies, including Paymaster.co, buy structured settlement payment rights. While there are fewer factoring companies in this market than two or three years ago, a majority of them are listed below.

Rates That Structured Settlement Companies Charge

Structured settlement companies are commonly known to charge somewhere between 9% to 18% percent of the value of future payments when working with someone selling settlement payment rights. This percentage is known as the discount rate. The discount rate is used to cover their operating costs, the risk from the annuity contract, and turn a profit.

Structured settlement buyers will pay you, your loved one, or your client less than the present value of the future payments. Otherwise, this secondary market would not exist. A review of Better Business Bureau complaints and feedback left on other review websites tend to show disappointment around lump sum payments that people received. This holds true for members of the National Association of Settlement Purchasers, the professional trade organization for structured settlement buyers. Compare quotes and work with a finance professional who prioritizes your financial security in order to try and get the best deal. If you want to receive the full value of your future payments then you must wait the entire period of time over which payments are scheduled.

How to Work With a Structured Settlement Buyer

- Contact a structured settlement company They will work with you to gather the necessary information about your structured settlement.

- Receive a quote After receiving the details of your structured settlement, you will receive a free quote to buy your structured settlement payment rights.

- Make a decision After considering our quote, if you decide to move forward with us, you would sign a contract and we would begin the process. Also, if you request a cash advance with your sale, you would receive it at this point.

- Attend a hearing In most states, the sale request will have to be approved by a court. It is extremely unlikely that the purchasing company that you work with will require you to pay for attorney fees out of pocket. You will need to attend the hearing and explain your decision to sell your structured settlement payments. Specifically, you need to demonstrate that you and your family can meet your financial needs if you sell your structured settlement payment rights. If you receive court approval, the approved transaction order will be forwarded to the insurance company.

- Receive your lump sum payment You will receive your payout distribution from your secondary market purchasing company.

Financial security will vary based on your financial needs. Do you expect ongoing medical bills following a workers’ compensation or personal injury claim? Your needs will differ from someone who lost a working family member and receives monthly payments from a wrongful death claim. Please consult a certified financial advisor or attorney who is experienced with annuity payments, also known as periodic payments, before making a decision.

Companies With Low Offers

Speaking with and receiving a quote from multiple companies may highlight that one or two of the offers pay much less money than the money offered by other buyers. Showing a reasonable offer to a company that proposed an unfairly low offer may lead to that lowballing entity coming close to or even beating the fair offer. What is more valuable in this case, selling payment rights to a company that was fair from the beginning or the company made an unfair offer before making a better offer?

The Best Structured Settlement Companies

- Paymaster.co Rating: 9.8 888-999-8606

- Annuity.org Rating: 9.6

- Fairfield Funding Rating: 9.3

The best structured settlement companies are those that provide the services that they promise. Meaningful company ratings do not exist because the companies that provide them are either buyers or stand to earn money from companies that buy payment rights.

We’ve compiled both a list of firms and their contact information that may be the most comprehensive list of settlement buyers on the web. We even rated some of them. Guess what? Paymaster.co is the rated at the top of the list because we are biased. Are we the best? We try to be. Is number two on our list better than number three? Maybe. They provide helpful information on their website. A lot of companies can provide a lump sum of cash. Humbly we’d love to have a chance to discuss what we can do for you.

Inclusion on this list is not an endorsement of any firm. Rating numbers or lack of ratings do not indicate anything negative. Given that every situation is unique, it will be up to you to decide which company is the best for you. There are a number of factors that you may consider. Here are a few that are probably important:

- Your Offer How do the terms the company offers you compare with terms offered by others?

- Customer Service How does the company treat you? With friendliness, patience, and understanding?

- Red Flags Do you have any reason to question or doubt the financial standing of the company?

More Structured Settlement Companies (Buyers)

PAYMASTER.CO

Call 1-888-999-8606

Website: https://paymaster.co

6230 Wilshire Blvd,

Suite 1795

Los Angeles, CA 90048

ANNUITY.ORG

189 S. Orange Ave,

Suite 1600

Orlando, FL 32801

Email: webmaster@annuity.org

Website: https://www.annuity.org

DRB CAPITAL LLC

1625 S Congress Ave,

Suite 200

Delray Beach, Florida

Phone: 888-981-8703

866-356-4610

Website: drbcapital.com

FAIRFIELD FUNDING

Phone: 855-296-0985

Fax: 888-857-4156

Email: info@fairfieldfunding.com

Website: fairfieldfunding.com

J.G. WENTWORTH

Phone: (866) 930-6480

Email: information@jgwentworth.com

Website: jgwentworth.com

201 King of Prussia Road,

Suite 501

Radnor, PA 19087

LIIBERTY SETTLEMENT FUNDING

Phone: (855) 643-0333

(855) 285-4158

Email: info@libertysf.com

Website: libertysettlementfunding.com

1855 Griffin Road

Suite B354

Dania Beach, FL 33004

CBC SETTLEMENT FUNDING

181 Washington Street,

Suite 375

Conshohocken, PA 19428

Phone: 800-843-9020

Email: info@cbcsettlementfunding.com

Website: cbcsettlementfunding.com

AMERICAN EQUITY FUNDING

7005 Alma Highway

Van Buren, Arkansas 72956

Phone: 800-874-2389

479-632-0851

Email: aefinc@americanequityfunding.com

Website: americanequityfunding.com

ANNUITY TRANSFERS, LTD.

1800 Preston Park Blvd.

Suite 115

Plano, TX 75093

Phone: 972-952-0260

888-638-0900

972-510-8288

Website: annuitytransfers.com

CLIENT FIRST SETTLEMENT FUNDING LLC

301 Yamato Rd #3200

Boca Raton, Florida 33431

Phone: (888) 594-1195

Website: clientfirstfunding.com

CROWFLY

Email: info@crowfly.com

Website: crowfly.com

Phone: 833-276-9359

FIRST STRUCTURED SETTLEMENT

Phone: 888-404-4242

FORTUNE SETTLEMENT SOLUTIONS

Phone: 833-736-7886

Email: info@fortunesettlements.com

Website: fortunesettlements.com

GLOFIN FUNDING

Phone: 888-667-1991

Fax: 888-317-0260

Email: info@glofin.com

Website: glofin.com

6905 Northcross, Dr

Suite 300

Huntersville, NC 28078

MAINSTREET FUNDING

Phone: 404-855-3330

Toll free: 877-919-8003

Website: mainstreetsettlement.com

197 West Crogan Street

Lawrenceville, GA 30046

NOVATION SETTLEMENT SOLUTIONS

Phone: 888-979-3740

Website: novationsettlementsolutions.com

1641 Worthington Road,

Suite 410

West Palm Beach, FL 33409

RSL FUNDING

Phone: 800-543-6513

Website: rslfunding.com

1980 Post Oak Blvd, Ste 1975

Houston, TX 77056

SENECAONE

Phone: 800.513.1394

301-913-9131

Email: inquiries@senecaone.com

Website: senecaone.com

Corporate Headquarters

7920 Norfolk Ave.

Suite #300

Bethesda, MD 20814

Florida Office

105 South Narcissus Avenue,

Suite 710

West Palm Beach, FL 33401

SETTLEMENT CAPITAL CORP.

Phone: 800-959-0018

Email: info@setcap.com

Website: settle4cash.com

14755 Preston Rd.,

Ste. 610

Dallas, TX 75254

STONE STREET CAPITAL, LLC

Phone: 301 951 8900

Email: info@stonestreet.com

Website: stonestreet.com

7316 Wisconsin Avenue

Fifth Floor

Bethesda, MD 20814

STRATEGIC CAPITAL

Phone: 866.256.0088

Email: info@StrategicCapital.com

Website: strategiccapital.com

575 Madison Ave

Ste 1006

New York, NY 10022-2511

Will the Court Approval Your Structured Settlement Transaction?

Whether the court approves your structured settlement buyout depends on a number of factors, similar to any other legal outcome:

- Does your judge usually approve or deny offers to purchase settlement payment rights? Judges and people and we all have biases.

- Is that amount of cash that you sacrifice in the deal unbelievably bad?

- How significant is your need for the cash that you would receive if you are allowed to sell your payment rights?

- Does a third party submit a filing and offer in your case that is much better than what was originally offered? If so, does the judge feel stronger about abiding by the terms of the deal that you accepted or about helping ensure that you get the best possible cash offer?

Companies That Buy Lottery Winnings

PAYMASTER.CO

Phone number: Call 1-888-999-8606

Paymaster.co buys lottery payments from people who want or need a lump sum cash payment upfront instead of regular annuity payments. Please contact our team for a no-obligation quote.

PEACHTREE FINANCIAL SOLUTIONS

1200 Morris Drive

Chesterbrook, PA 19087

Website: peachtreefinancial.com

J.G. WENTWORTH

201 King of Prussia Road,

Suite 501

Radnor, PA 19087

Website: jgwentworth.com

What is a Structured Settlement Annuity Company?

A structured settlement annuity company is an insurance company that issues payments according to settlement agreements on behalf of defendants or their insurers. These annuities must be purchased from licensed structured settlement brokers or planners.